When you’re keen to build up your savings it’s all too easy to put it off until you get that next payrise. But while it seems common sense that earning more money is the best way to increase your savings, that often isn’t the case. In fact, decreasing your spending can have a much bigger impact on the health of your personal finances.

Earning More Doesn’t Always Equal Saving More

There are two key factors which can mean an increase to your pay packet doesn’t have the same effect to your savings as you thought it might.

1 – Lifestyle Inflation – As our earnings increase we typically experience lifestyle inflation – increasing spending because we have more money available. For example in a low paid job you may choose to spend £400 on a budget holiday, whereas that may increase to £1000 as your disposable income increases.

2 – Increases Aren’t Always As Big As They Seem- If you’re on a medium to high salary you may find that a lot of the additional money you would earn through a payrise will disappear through income tax, National Insurance (NI) and student loan repayments.

Below is approximately how much money you would receive in your take home pay for a pay rise of £1000.

| Tax Band | Tax Rate | Tax Deduction | NI Deduction | Take Home Pay |

|---|---|---|---|---|

| Personal Allowance: Up to £11,850 | 0% | £0 | £0* | £988 |

| Basic Rate: £11,851 to £46,350 | 20% | £200 | £120 | £680 |

| Higher Rate: £46,351 to £150,000 | 40% | £400 | £20 | £580 |

| Additional Rate: Over £150,000 | 45% | £450 | £20 | £530 |

Reducing Your Spending Increases Savings Twofold

Reducing the amount you regularly spend has a double impact, as it increases the amount you can put into savings, while decreasing the amount you need to live on in the future. For those who are building towards a goal of financial independence this can be very powerful!

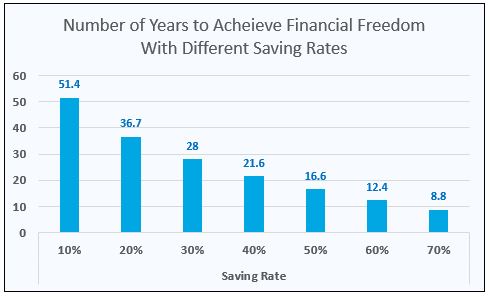

The below graph demonstrates how increasing your saving rate quickly reduces how long it takes to build up enough money to sustain yourself forever. The figures are taken from the Networthify early retirement calculator and are true regardless of whether you have a salary of £15,000 or £50,000!

So rather than delaying building up your rainy day fund, get started today by finding ways to reduce the money you spend. Check out this post for 50 ways to spend less money or create your own custom pie chart to work out where your money goes.

When you do experience salary increases remember not to become subject to lifestyle inflation. An easy way to avoid this is to set up a standing order from your current account to your savings account straight after payday. Alternatively you may wish to use the extra money to increase your pension contributions.

Have you ever fallen prey to lifestyle inflation or do you have any tips to avoid it? Let me know in the comments!